Over 5,000 companies will be required to report greenhouse gas (GHG) emissions under California Senate Bill (SB) 253—starting in 2026 for fiscal year (FY) 2025 emissions.1 This law requires U.S. companies doing business in California with more than $1 billion of annual revenue to follow the GHG Protocol, which is an internationally recognized standard for reporting GHG emissions. Many companies subject to this law will be reporting their GHG emissions for the first time and may be unfamiliar with GHG Protocol.

Here are the fundamentals of the GHG Protocol and what organizations should know when reporting GHG emissions.

GHG Protocol Background

The GHG Protocol is the world’s most widely used GHG accounting standard. In addition to California’s SB 253, the GHG Protocol is the underlying standard referenced in the SEC’s proposed climate disclosure rule and proposed federal contractor GHG reporting rules.

While the GHG Protocol has more than a dozen documents for GHG accounting, the key documents for SB 253 are:

- Corporate Accounting and Reporting Standard – provides overall requirements for preparing a GHG emissions inventory, including Scope 1 emissions2

- Scope 2 Guidance – describes how to measure and report emissions from purchased or acquired electricity, steam, heat, and cooling3

- Scope 3 Corporate Value Chain Standard – addresses how to calculate indirect upstream and downstream value chain emissions4

- Scope 3 Calculation Technical Guidance – provides methods and examples for calculating each of the 15 Scope 3 categories5

Under CA 253, Scope 1 and 2 need to be reported starting in 2026 for FY 2025 emissions with a phase-in requirement to report Scope 3 emissions starting in 2027 for FY 2026.

Scope 1 Emissions

Scope 1 emissions are direct GHG emissions that stem from sources a reporting entity owns or directly controls, regardless of location. Scope 1 breaks down into four categories:

| Category | Definition |

|---|---|

| Stationary combustion | Emissions from fuel burned in stationary, e.g., furnaces, generators, and engines |

| Mobile combustion | Emissions from fuel burned during transportation, e.g., cars, trucks, and airplanes |

| Process emissions | Emissions from physical or chemical processes, e.g., steel, cement, or ammonia production processes |

| Fugitive emissions | Intentional and unintentional releases of GHGs, e.g., refrigerant leakage from air conditioning |

Most companies have Scope 1 emissions. For example, financial services companies often have stationary emissions from central heating furnaces burning natural gas, fugitive emissions from air conditioning refrigerant leakage, and mobile emissions from company vehicles.

Scope 2 Emissions

Scope 2 emissions are indirect GHG emissions from consumed electricity, steam, heating, or cooling purchased or acquired by a reporting entity.

There are two Scope 2 accounting methods:

- Location-based – Averaged emissions intensity of the electricity grids where the energy consumption occurs.

- Market-based – Emissions from electricity that companies have chosen through contractual instruments, such as power purchase agreements and renewable energy certificates.

The Scope 2 standards require reporting using both location- and market-based methods for companies with operations in markets with electricity contractual instruments, including but not limited to the following geographies:

- United States

- European Union

- Most Latin American countries

- India

- Japan

Organizations must identify what electricity data and emission factors are used. The standards include emissions factor hierarchies based on precision. Emission factors are regularly updated; GHG Protocol recommends that a public emissions inventory “be based on the best data available at the time of publication, while being transparent about its limitations.”6

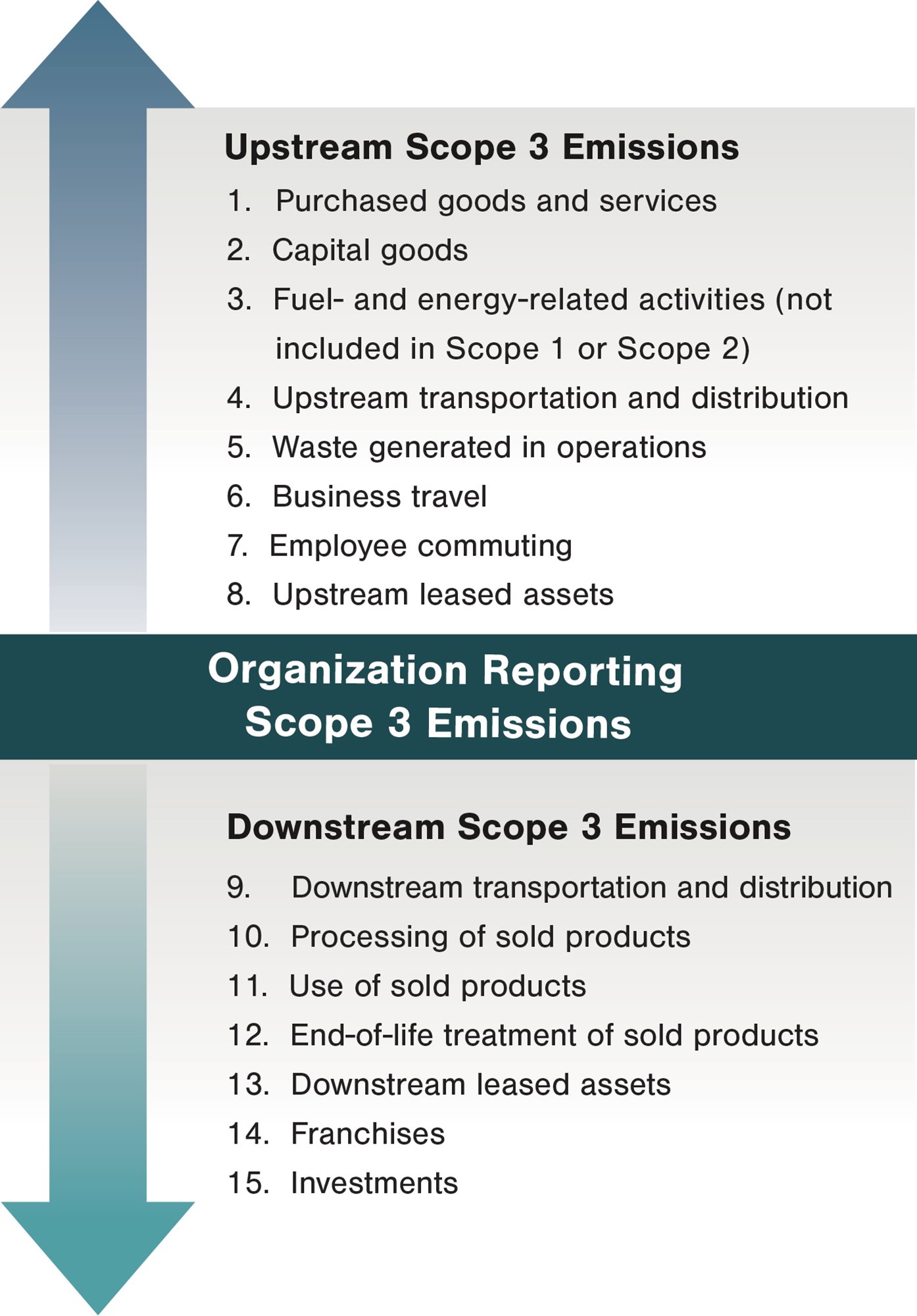

Scope 3 Emissions

Scope 3 emissions are indirect upstream and downstream GHG emissions, other than Scope 2, from sources that the reporting entity does not own or directly control.7

- Organization Reporting Scope 3 Emissions

- Upstream Scope 3 Emissions

- Purchased goods and services

- Capital goods

- Fuel- and energy-related activities (not included in Scope 1 or Scope 2)

- Upstream transportation and distribution

- Waste generated in operations

- Business travel

- Employee commuting

- Upstream leased assets

- Downstream Scope 3 Emissions

- Downstream transportation and distribution

- Processing of sold products

- Use of sold products

- End-of-life treatment of sold products

- Downstream leased assets

- Franchises

- Investments

- Upstream Scope 3 Emissions

Companies need to determine which Scope 3 categories are relevant to their organization using multiple criteria spelled out in the standards. Then, data collection plans and calculation methodologies should be established for the relevant Scope 3 categories.

Company Adoption of the GHG Protocol to Prepare for SB 253

Companies reporting to the GHG Protocol commonly encounter challenges. For example, sustainability professionals routinely struggle with knowing which emission factors to use—often relying on outdated or poorly sourced values. Respondents might incorrectly report Scope 3 data by highlighting categories that are not relevant to their business model or failing to account for material Scope 3 categories. Similarly, as organizations mature and new data becomes available, sustainability professionals could identify the need to restate previously reported emissions values. Companies need to be careful to follow the restatement requirements in the GHG Protocol closely as failure to do so could easily lead to misinterpretation and potentially regulator-imposed penalties. To prepare for SB 253, organizations must understand that GHG accounting is inherently cross-functional. Due to the nature of GHG accounting, individuals in financial accounting, facilities management, supply-chain management, and human resources should be involved. A point person within the organization should be quickly identified, and that individual needs to be prepared to deliver clear communication to many stakeholder groups on data and auditability requirements in alignment with the GHG Protocol and SB 253. To encourage completeness and accuracy of the data, organizations may even want to select a carbon accounting software that can help GHG accounting professionals review alignment with the GHG Protocol. Such decisions could help organizations prepare for third-party assurance requirements that come into effect in FY 2026. Creating the momentum in understanding SB 253 means that organizations will need to become knowledgeable of the GHG Protocol standards in the same way that companies require accounting professionals to be aware of accounting standards. GHG accounting, just like financial accounting, requires a strong attention to detail and the ability to adapt to reporting requirements. And once organizations embrace the fundamentals of GHG reporting through the GHG Protocol, understanding SB 253 will be as easy as 1-2-3.

See our related FORsights™ for more information:

- California Enacts GHG & Climate Reporting Laws Requiring Major Action by US Companies

- Attestation and Internal Control Considerations for ESG Programs

- Five Critical Insights in Applying COSO’s Guidance for ICSR

- Behind the Curtain: What You Need to Know About ESG Assurance

- 1Climate Corporate Data Accountability Act, California HSC §38532, 2023.

- 2The Greenhouse Gas Protocol, A Corporate Accounting and Reporting Standard, Revised Edition, World Resources Institute and World Business Council for Sustainable Development, March 2004.

- 3The Greenhouse Gas Protocol, Scope 2 Guidance, An Amendment to the GHG Protocol, World Resources Institute, 2015

- 4The Greenhouse Gas Protocol, Corporate Value Chain (Scope 3) Accounting and Reporting Standard, Supplement to the GHG Protocol Corporate Accounting and Reporting Standard, World Resources Institute and World Business Council for Sustainable Development, September 2011.

- 5The Greenhouse Gas Protocol, Technical Guidance for Calculating Scope 3 Emissions, Supplement to the Corporate Value Chain (Scope 3) Accounting & Reporting Standard, World Resources Institute and World Business Council for Sustainable Development, 2013.

- 6The Greenhouse Gas Protocol, A Corporate Accounting and Reporting Standard, Revised Edition, World Resources Institute and World Business Council for Sustainable Development, March 2004.

- 7Climate Corporate Data Accountability Act, California HSC §38532, 2023.