- Clean firm assets include technologies that are weather independent, like hydrogen, geothermal, nuclear, and carbon capture.

- Benefits of these options include a cheaper overall system, fewer infrastructure and transmission needs, and less risk from geopolitical and pricing changes, as well as flexibility as they function independent of weather or seasonal shifts.

- Even so, many clean firm assets are not commercially scalable, and they require long lead times with some public skepticism about development.

- Clean firm assets could be included as part of the mix of a diversified energy solution to reduce risk and cost while providing “backup capacity.”

Clean energy is frequently perceived as solely solar and wind—and often with good reason. Some projections estimate that 60% of the U.S.’ energy will come from solar and wind by 2035.1 Even so, with the dramatically rising energy demand in the U.S. driven by data center development and more, other forms of clean energy should enter the discussion. “Clean firm assets” is a “catch-all term for weather-independent clean resources that can be turned on and off at will.”2 Including technologies like nuclear fission or fusion, hydrogen, geothermal, and carbon capture paired with biomass or fossil fuels,3 clean firm assets may prove to be critical in the long-term strategy of the nation’s energy mix.

What Are Clean Firm Assets?

While many are accustomed to seeing a solar field or wind turbine, there is less familiarity with other forms of clean energy. As mentioned previously, this bucket of “everything else” is commonly referred to as “clean firm assets.” While renewable energy sources like solar and wind are categorized based on their “limitless” nature, clean energy overall is more focused on greenhouse gas emissions and sustainability. Johns Hopkins University describes sustainable energy as “com[ing] from sources that can fulfill our current energy needs without compromising future generations.”4 Therefore, not all renewable energy sources are necessarily sustainable.

This distinction was a driver for the One Big Beautiful Bill Act (OB3), as the ability for clean firm assets to qualify for the investment and production tax credits (meaning, in part, that they have a “greenhouse gas emissions rate … not greater than zero”5) was largely unchanged (with the exception of solar and wind) by the legislation. The listing of clean firm assets is generally considered to “include nuclear fission, nuclear fusion, fossil generation with high levels of carbon capture and upstream methane mitigation, combustion or gasification of sustainably sourced biomass with high levels of carbon capture and storage, low-emission (e.g., hydrogen) fuel combustion, and geothermal.”3

Which Kinds of Clean Firm Projects Are Being Developed?

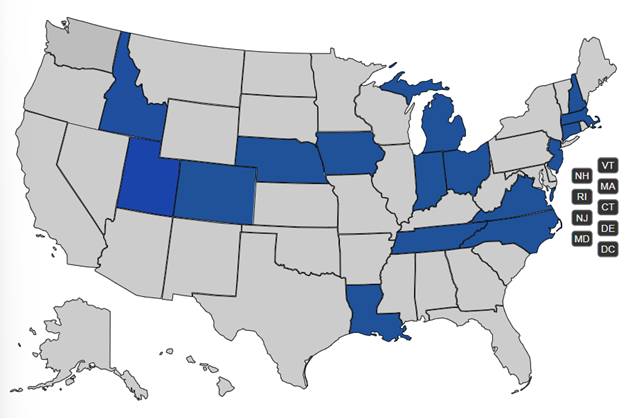

Therefore, in theory, there are a lot of options. So, which is the frontrunner? The answer is complicated and dependent on the location, time frame, and appetite for policy change surrounding each technology. For example, in the southeastern United States, nuclear fission has been the most prevalent clean firm asset, with projects like Plant Vogtle Unit 4, an expansion of the existing plant by an additional 1,114 megawatts (MW) becoming operational in Georgia in 2024 (total nameplate capacity is now nearly 5 gigawatts), and in March 2026, a $40 billion deal was announced with Japan to build “small modular reactors in Tennessee and Alabama.”6 Nuclear also seems to be supported by state policy change. The NARUC-NASEO Advanced Nuclear State Action Tracker provides an interactive map that “focuses on highlighting advanced nuclear activities and partnerships involving state government entities (i.e., State Public Utility Commissions, State Energy Offices, state legislatures, and Governor’s Offices).”7 The following graphic provides insight into which states have legislation to include nuclear projects within the category of clean energy, an indicator that these states may support financing and providing other resources to these projects.

Source: NARUC-NASEO Advanced Nuclear State Action Tracker. National Association of Regulatory Utility Commissioners. Map last updated on September 5, 2025.

Other technologies are being explored but are currently less broadly commercialized. Hydrogen has been discussed, though regulations and policy changes have caused some level of hesitation in the space. Even so, there are a number of notable hydrogen projects proposed and underway in the United States. Duke Energy has “unveiled its DeBary Hydrogen Production Storage System in Volusia County, the first demonstration project in the United States capable of using an end-to-end system to produce, store and combust up to 100% green hydrogen.”8 In Utah, the Intermountain Power Project (IPP) will transition from a coal-fueled power plant to a green hydrogen-powered facility.9

Multiple carbon capture and storage (CCS) projects are active in Louisiana,10 and in California, the Carbon TerraVault project aims to develop “CCS and direct air capture plus storage (DAC+S) projects that inject CO2 captured from industrial sources into depleted underground reservoirs and permanently store CO2 deep underground.”11 Alternatively, geothermal energy can be used for electricity generation, heating and cooling, or direct use. Utilizing hot water from deep reservoirs, drilling for these resources can allow for heat that powers turbines. District heating and cooling systems allow for larger scale geothermal heat pump implementation. As an example, in 2023, an “enhanced geothermal” plant came online to provide Nevada’s grid electricity.12

All of these examples say that clean firm development is a reality and is “expected to be particularly important in regions of the country where wind and solar resources are less competitive, and essential for decarbonizing several nonelectric sectors of the economy.”13 The Corporate Energy Buyers Association’s deal tracker reports that from 2021 to Q3 2025, there have been the following clean firm announcements:14

| Type of Clean Firm Asset | # Projects | Locations |

|---|---|---|

| Nuclear | 9 | PJM, Northwest, ERCOT, MISO, Southeast, Undisclosed |

| Hydro | 4 | PJM |

| Geothermal | 4 | Southwest, Undisclosed |

| Fusion | 4 | PJM, Northwest, Undisclosed |

What Are Some Benefits of Clean Firm Assets?

Research has shown that clean firm assets have their unique contributions to the clean energy space. These include:

- Achieving decarbonization has been shown to be more affordable overall when including clean firm assets.

- Clean firm assets can reduce the scale of infrastructure buildout needed for decarbonization, including long-distance transmission and energy storage.

- Unlike some energy alternatives, clean firm assets are not affected by the time of day, weather, or seasonal patterns.

- Use of clean firm assets can mitigate risk stemming from geopolitical situations, price fluctuations, supply chain constraints, regulation hurdles, and more.

It is generally understood that on an asset-by-asset basis, it is currently cheaper and quicker to build a solar or wind facility than a clean firm asset facility. In fact, the U.S. Energy Information Administration (EIA) demonstrates that capital cost per kilowatt for solar photovoltaic (PV) with single-axis tracking is $1,502, while geothermal is $3,963, advanced nuclear (Brownfield) is $7,861, and a biomass plant with 95% carbon capture can be as high as $12,631. However, when looking at the broader effort toward decarbonization, “studies consistently show that achieving 100% decarbonization is cheaper with clean firm resources.”15 In fact, a study focused on California showed “that a diverse portfolio of wind, solar, storage, and multiple sources of clean firm generation could deliver electricity at ‘about one-third less than the cost of an all-wind-and-solar approach.’”16 Other sources report a 40 to 65% decrease in costs due to the integration of clean firm assets in decarbonized electricity system models.17

How is this cost savings possible? Perhaps most foundationally, clean firm assets are more efficient. Said another way, they receive a better utilization rate: “clean firm resources generally operate at higher utilization rates (50-100%) than variable renewables (20-50%), requiring less total generating capacity to produce the same amount of energy and less transmission capacity to carry it.”16

In addition, clean firm assets have been shown to reduce infrastructure buildout needs, especially when considering long-distance transmission and energy storage development. For example, the Net Zero America study “found that 1 GW of clean firm capacity offsets roughly 5-8 GW of variable renewable and storage capacity needs. These impacts apply also to transmission, where clean firm buildout modeled in Net Zero America more than halved total transmission buildout needs.”16 Generally speaking, wind and solar projects aren’t located by electrical users, primarily due to the cost and availability of the land needed to support the project. Instead, these projects rely on long-distance transmission systems to get the power to more populous areas. In reality, however, dependency on these transmission systems presents significant timing delays due to siting and permitting issues. Clean firm assets do not require such long-distance transmission systems, which avoids both these timing issues and the cost of the infrastructure itself. When it comes to energy storage, while current battery systems offer shorter-term storage solutions, they are not built to combat the seasonal or weather impacts on solar and wind technologies in the longer term.

This immunity to weather, time of day, and seasonality impacts is possibly the most obvious benefit of clean firm assets. By being more consistent in this way, the use of clean firm assets could act as a backup reserve for times with low sun and wind. Without it, utilities may implement excess solar and wind facilities to increase resiliency and offset these periods of need. The same goes for additional storage capacity, which helps with energy reliability but could be largely unused in times of ample sun and wind. Either way, excess renewables and storage add to overall cost and could impact the price tag of energy for ratepayers.

Ultimately, the use of clean firm assets helps to mitigate risk. Diversification in power sources combats potential issues with supply chain and the availability of certain technologies. Similarly, clean energy solutions are not susceptible (depending on the technology) to geopolitical impacts and price fluctuations of oil.

What Are Some Challenges With Clean Firm Assets?

So why aren’t clean firm assets more prevalent now? They currently face some significant barriers to widespread implementation. Duke University’s Nicholas Institute for Energy, Environment & Sustainability outlines the reasoning for this quite succinctly: “These technologies are at varying stages of commercial readiness, including some that face significant deployment barriers such as cost premiums, long lead times, technology-specific siting and permitting hurdles, and supply chain disruptions.”3 Said another way, they are expensive, they aren’t easily scaled, they take a while to build, and there is still room for public acceptance and policy support.

Some of the technologies best perform with specific infrastructure, much of which is not widely available. For example, “carbon capture and storage, for instance, are typically more cost-effective when they can connect to an established CO2 pipeline network or trunk line rather than building their own transportation and storage infrastructure.”16 Hydrogen facilities present a similar issue.

Another challenge is more practical, and it’s the reality that most developers plan projects within a 10-year window. Development of many of these clean firm asset facilities would take much longer than that. Therefore, these projects tend to be sidelined to focus on the cheaper and more quickly implemented alternatives of solar and wind. When coupled with variability in state policy and permitting issues, it makes widespread deployment of clean firm assets difficult. For technologies with some proven success—like nuclear—the result is stymied growth, while for less proven asset types—like hydrogen—it’s hard to get funding or support for the technology itself (and the accompanying infrastructure) to progress. This cycle has been described as a “negative feedback loop where near-term deployment deficiencies result in stagnant technological progress and continued perceptions of financial risk, further stunting deployment.”16

The Solution or the Safety Net?

The practical limitations of wide implementation of clean firm assets begs the question: is it better to depend solely on renewables, solely on clean firm assets, solely on traditional energy (like oil and gas), or on a mix of all three? Many opine that given all of the competing micro and macroeconomic forces at play, this “mix” approach is likely the most beneficial. While solar and wind could be built at a relatively low cost in the near term, developers could start building clean firm facilities to support these renewable projects in times where weather impacts power production. In this model, they are not the primary source of consistent power but could be used flexibly as needed. In short, clean firm assets would act as a safety net. A Senior Fellow at Energy Innovation, Eric Gimon, states, “Day to day, you need good brakes that won’t fail, but you also want a seatbelt and an airbag even if they are not used all the time.”15 That being said, it’s possible that fossil-fueled generators could also serve in this “backup” role for capacity with relatively low emissions.1

This exercise of longer-term facility planning benefits from an exercise of modeling cash flows, clean energy credits, risks, supply chain availability, tariffs, and more. Reach out to an experienced professional at Forvis Mazars today to explore further.

- 1Paul Denholm, Ilya Chernyakhovskiy, Lauren Streitmatter. “Maintaining Grid Reliability—Lessons from Renewable Integration Studies.” National Renewable Energy Laboratory. April 2024.

- 2Michelle Solomon. “Clean firm generation is an important piece of the energy transition, but it’s no silver bullet.” Utility Dive. December 5, 2025.

- 3Cobb, P. L., A. Hopkins, T. Profeta, and J. Tarr. 2025. “The Role of Clean Firm Power in a Reliable, Affordable, and Clean Electricity System in the Southeast.” NI PB 25-06. Durham, NC: Nicholas Institute for Energy, Environment & Sustainability, Duke University.

- 4“Renewable Energy vs. Sustainable Energy: What’s the Difference?” Johns Hopkins School of Advanced International Studies. April 30, 2025.

- 5Section 45Y(b)(1)(A)(iii).

- 6Franklin, Mariah. “Japan invests up to $40B in Tennessee and Alabama nuclear reactors.” Knox news. April 3, 2026.

- 7NARUC-NASEO Advanced Nuclear State Action Tracker. National Association of Regulatory Utility Commissioners. Accessed April 9, 2026.

- 8Anton, Ben. “Duke Energy Unveils Nation’s First System For Producing, Storing and Combusting 100% Green Energy.” Renewable Energy Magazine. January 8, 2026.

- 9“Conversion of Intermountain Power Project to Green Hydrogen.” Green Hydrogen Coalition. Accessed April 9, 2026.

- 10“Expanding our CCS operations in Louisiana with another project startup.” ExxonMobil. February 18, 2026.

- 11“Carbon Terravault, Committed to Our Net Zero Future. California Resources Corporation.” Accessed April 9, 2026.

- 12Gallucci, Maria. “America’s first ‘enhanced’ geothermal plant just got up and running.” Canary Media. November 28, 2023.

- 13Bruce Phillips, Neil Fisher, Anjie Liu. “Review and Assessment of Literature on Deep Decarbonization in the United States: Importance of System Scale and Technological Diversity.” The NorthBridge Group. April 20, 2021.

- 14“Mapping the Momentum: Where Clean Firm Energy is Taking off and Who’s Behind It.” CEBA. December 9, 2025.

- 15Michelle Solomon, Sara Baldwin. “Grid Reliability in the Clean Energy Transition.” Energy Innovation. February 2025.

- 16“Policy Opportunity Brief: Clean Firm Power.” Center for the New Energy Economy. 2025.

- 17Kasparas Spokas, Wilson Ricks. “Clean Firm Electricity Technologies: What, Why, How.” Clean Air Task Force. February 2026.