One trend is clear—the U.S.’ energy demand is increasing, largely due to the trajectory of data center development. Less apparent, however, is where these data centers will be built and how they will be powered. The industry is trending toward an “all of the above” approach1 to generating power for these centers, putting in place clean energy technologies in addition to traditional gas. The catch is that tax credits for clean energy are phasing down and changing. Clean energy developers are faced with long interconnection times and permitting issues; and some technologies require geographies with large amounts of land. Simultaneously, data center property prices are skyrocketing in populated infill areas. As a result, there appears to be an opportunity and trend for data center and clean energy developers to move to rural tertiary markets for new construction. The kicker? Some of these locations may be classified as rural opportunity zones, providing added incentives for selecting these locations.

Background

According to the American Edge Project, in winter 2025, there were “4,149 active data centers across the United States, with another 2,788 announced or under construction. When completed, the U.S. will have nearly 7,000 data centers—a jump of 67 percent.”2 In addition to the computing hardware, data center spending will be directed toward electrical equipment, power generation, network infrastructure, land acquisition, and storage—ultimately involving those in the construction, power, and manufacturing industry simultaneously. By 2031, the U.S. data center construction market is expected to reach $23.74 billion, an uptick from $15.51 billion in 2026.3 What comes with this is an uptick in energy demand, with the U.S. Department of Energy reporting that “data center load growth has tripled over the past decade and is projected to double or triple by 2028.” This equates to 12% of total U.S. electricity (580 TWh) by that time.

Clean energy alternatives are playing a role in filling this rising energy demand. Even so, the clean energy industry has been facing challenges from multiple fronts—tax, regulatory, or otherwise. The One Big Beautiful Bill Act (OB3) changed the timing of tax credits for solar and wind, while implementing what is colloquially known as the “Foreign Entity of Control” requirements across the board. The industry is also facing prohibitively long interconnection wait times, as well as juggling permitting and zoning roadblocks. Even so, meaningful tax credits—for clean energy developers, manufacturers, and developers—remain (usually at around 30%), with the technologies providing flexibility to data centers for their energy demands.

The OB3 also introduced the concept of a qualified rural opportunity zone fund (QROF), which is essentially a qualified opportunity zone (QOZ) located in certain rural areas with additional tax benefits. As of September 2025, the IRS identified 3,309 of the 8,764 QOZs to be comprised entirely of a rural area. As detailed in our FORsights™ article on the topic, a QROF “allows for a 30% basis step-up after being held for five years, and a reduced 50% substantial improvement requirement. Generally, the QROF rules are effective January 1, 2027; however, the 50% substantial improvement requirement is effective on July 4, 2025.”

The “All-of-the-Above” Approach to Energy Demand

As evidenced recently, depending solely on traditional oil and gas to support the U.S.’ energy demand leaves the country vulnerable to fluctuations in gas prices and availability. Globally, according to the International Energy Agency (IEA), “through 2030, electricity consumption is projected to grow at least 2.5 times as fast as overall energy demand.”4 Therefore, developers are trending toward an “all-of-the-above” approach to power their data center projects. Leveraging renewable technologies like solar and wind, some are exploring “clean firm” solutions like carbon capture, nuclear, geothermal, and clean fuel as well.

This trend is not necessarily new. According to Pew Research, “As of 2024, natural gas supplied over 40% of electricity for U.S. data centers, according to the IEA.5 Renewables such as wind and solar supplied about 24% of electricity at data centers, while nuclear power supplied around 20% and coal around 15%.”6 In the longer term, the U.S. Department of Energy foresees deployment of advanced small modular reactors (SMRs) in the late 2020s to early 2030s, while CBRE views SMRs to be a part of the mix by 2035.7

What some of these energy alternatives require, however, is a longer timeline for development. A light-water nuclear plant can take up to 12 years,8 while solar PV and onshore wind (depending on size) can take around 2—4 years for commissioning.9 This is in comparison to the relatively shorter 18- to 24-month development timeline for data center construction itself.

Trending: Rural Development of Data Centers

Another constraint for clean energy power sources is the inherent land requirements for the facilities. According to the Solar Energy Industries Association, “a utility-scale solar power plant may require between 5 and 7 acres per megawatt (MW) of generating capacity.”10 When coupled with the fact that “average-sized data centers typically require about 5 to 10 megawatts (MW) of power annually, [and that] according to the International Energy Agency, larger “hyperscale” data centers that require 100 MW or more a year are becoming more commonplace,”11 that’s a lot of land in total for these data center facilities. It becomes even more problematic when considering that some data centers are required to pay a premium for land if located near end-users. For example, according to CBRE, recently the price tag comes in at $8 million per acre in Northern Virginia and the Northeast.

The result? Data centers are moving to rural locations with more space, lower prices, and more flexibility for power sources. Not all data centers need to be in populated areas—when artificial intelligence (AI) is in the process of being trained, it’s less crucial to be near end-users. Reuters includes Indiana, Wyoming, Ohio, and Louisiana as among the top 30 U.S. states for current and planned data center capacity12 —possibly to the relatively low cost of land and energy in the areas. To this point, quick power access is proving critical to site selection: “sites offering power access within 18 to 36 months for greenfield development are highly sought after, driving significant investment from owner-users and developers in tertiary markets.”

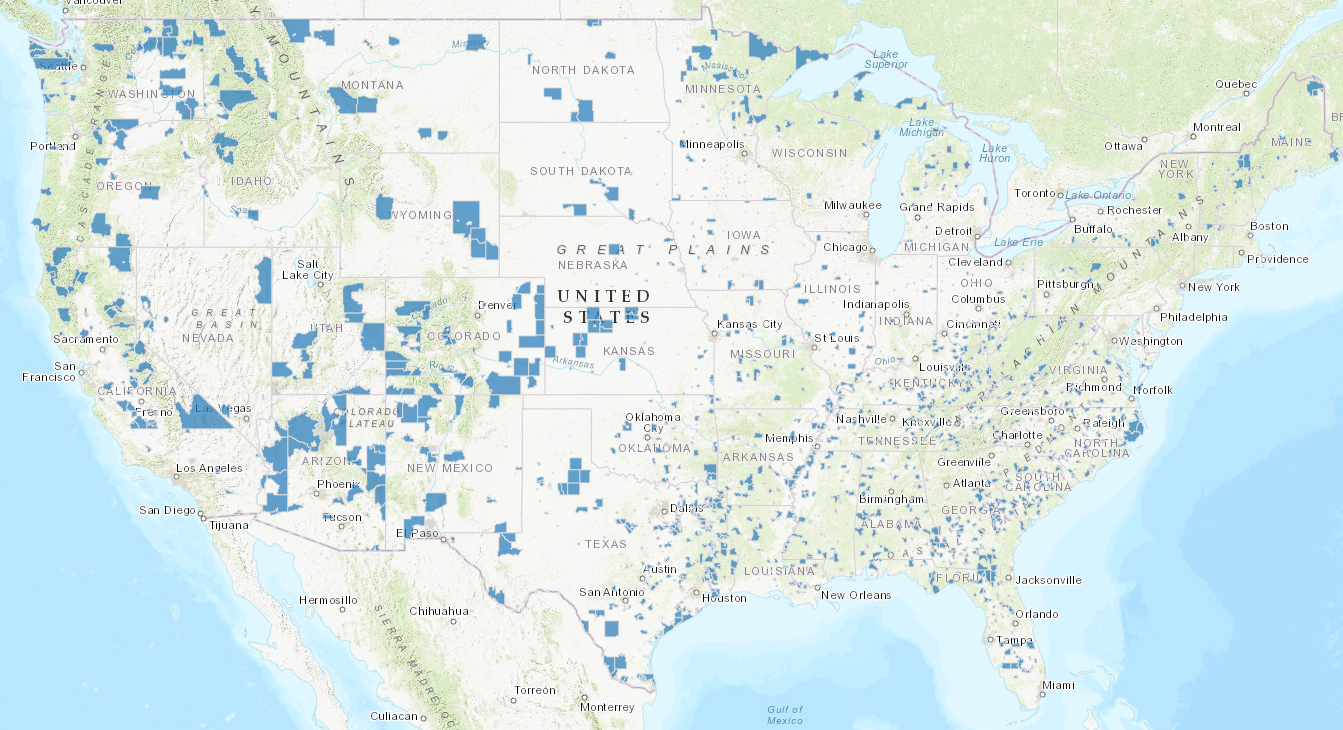

So where are these data centers being built? Virginia, Texas, and Arizona alone make up 2GW of the 15GW of national data center power capacity; planned increases are planned in less established states as mentioned above. When these locations overlay with the map of rural opportunity zones, the opportunity for additional tax incentives solidifies. As seen in the map below, large areas qualify for the QROF designation in the midwestern and western U.S., although there are smaller QROFs in higher concentrations along the east coast.

Source: Office of Policy Development and Research, March 23, 2026.

Source: Office of Policy Development and Research, March 23, 2026.

For the states previously mentioned with data center activity, the following applies in relation to the number of rural opportunity zones in each state, according to the filterable and interactive map available by the U.S. Department of Housing and Urban Development:

- Indiana—49

- Louisiana—70

- Wyoming—19

- Tennessee—87

- Ohio—92

- Mississippi—77

- California—130

- Virginia—95

- Texas—288

The other factor influencing site selection is state tax policy and other regulations, ranging from “income, sales, and property tax incentives”13 to electricity cost reduction.14 Requirements apply to obtain these benefits, e.g., investment thresholds, wage and job requirements, etc. Certain states are exploring legislation to overcome permitting and interconnection delays that could otherwise encourage developers to construct elsewhere.

The Broader Impact

Developers and investors in data centers located in QROFs and powered by clean energy find themselves in a unique situation. Not only may they be receiving tax incentives via the opportunity zone mechanism and clean energy credits, but they may also be able to play a part in generating tax revenue for the community, provide jobs, and help avoid any upcoming national energy deficit.

While the development of data centers has spurred political debate outside the scope of this article, the rate of new data center projects will require construction jobs—from engineers to contractors to utility workers and so forth. They also will generate tax revenue on an ongoing basis, with one source estimating up to $27 billion of state and local tax revenue nationwide over the next 10 years.

The efficacy of opportunity zones to accomplish the broader policy’s goals of bringing prosperity and housing to lower-income areas has been debated. However, observations have found “positive effects of Opportunity Zone designation on commercial real estate transactions, building permits, and construction employment.”15 In addition, at least in a metropolitan area, research has shown that “the OZ designation increased employment growth relative to comparable tracts by between 3.0 and 4.5 percentage points and new jobs were created across many different industries and education levels.”16 This same study—which occurred in 2021—did not show job growth in rural areas, but the research conducted was long before the creation of QROFs from the OB3 and their related tax benefits.

Barriers to Growth

Although there are these impacts both for developers and their surrounding communities, there are undoubtedly barriers as well:

- Not all data centers can be built in rural locations, with low latency infrastructure requiring closer proximity to users.

- All QROF benefits don’t begin until 2027, leaving a gap between the need for energy and AI with the availability of this incentive.

- Clean energy power facilities may not be built in time to support data centers, with utilities at times offering only incremental increases to power supply as they expand their own infrastructure.

- Permitting, zoning, and other regulatory roadblocks continue to persist, despite some states’ moves to rectify the issues.

- Tariffs are increasing costs of construction materials and imported energy technologies.

- Tax changes like Foreign Entity of Concern (FEOC) rules and timing adjustments for clean energy credits make clean energy development and investment more complicated.

Regardless, a look toward economic, energy, and policy trends provides the taxpayer with a unique opportunity for tax and strategic planning. While the overall energy demand of the U.S. rises—largely due to data center development—clean energy can play a role in meeting that demand, all while allowing for tax credits in certain situations. Locating these data centers in rural opportunity zones provides for additional tax incentives, while theoretically boosting the community and providing for flexibility in power sources. To learn more about tax strategies with QROFs and clean energy, or to explore planning opportunities for those in the infrastructure or real estate industries, contact an experienced professional at Forvis Mazars today.

- 1The “all-of-the-above” approach to energy is a colloquial phrase used to describe the use of diversified energy sources for power generation—from solar and wind, to nuclear and clean fuel, to traditional oil and gas (and more).

- 2American Edge Project. America’s AI Surge: Powering Investment, Jobs, and Growth in Every State. Winter 2025.

- 3United States Data Center Construction Market Size & Share Analysis-Growth Trends and Forecast 2026-2031. Mordor Intelligence. February 27, 2026.

- 4Eren Çam, Marc Casanovas, John Moloney, and Matthew Davis. Electricity 2026, Analysis and forecast to 2030. International Energy Agency. 2026.

- 5“Energy supply for AI,” iea.org, April 2025.

- 6Rebecca Leppert. What we know about energy use at U.S. data centers amid the AI boom. Pew Research Center. October 24, 2025.

- 7North America Data Center Trends H2 2025. CBRE. February 25, 2026.

- 8Ryan Mallory. Why Nuclear Power Is Most Viable Option for Data Centers. Power. March 12, 2026.

- 9Anurag Gumber, Riccardo Zana, Bjarne Steffen. A global analysis of renewable energy project commissioning timelines. Applied Energy. 2024.

- 10Land Use & Solar Development. Solar Energy Industries Association.

- 11Louise Poirier. Infographic: Data Center Power Needs Escalate. Mechanical Engineering Magazine.

- 12Gavin Maguire. Charting the data center development roadmap in key US states. Reuters. January 22, 2026.

- 13Scott Wright, Alla Raykin, Laurin E. McDonald. Tricks and Traps of Data Center State Tax Incentives. Tax Notes. January 1, 2024.

- 14Dan Thompson. State-level data center policies, then and now: Part 2, the Southeast. 451 Alliance. February 12, 2026.

- 15Matthew Freedman, Shantanu Khanna, David Neumark. The Impacts of Opportunity Zones on Zone Residents. Center for Economic Studies. June 2021.

- 16Alina Arefeva, Morris A. Davis, Andra C. Ghent, Minseon Park. Job Growth from Opportunity Zones. February 19, 2021.